Mortgage Rates & Bank of Canada, Mortgage Renewals 17 Jun 2026 Should You Choose a Variable Rate Mortgage in Ontario Right Now? Thinking about a variable rate mortgage? With Ontario rates shifting, find out if variable or fixed is the right choice for your renewal in 2026. Aman Harish No Comments

Debt Consolidation, Mortgage Renewals 15 Jun 2026 How to Handle a Mortgage Renewal Near Retirement in 2026 Facing a mortgage renewal near retirement in 2026? Learn how to handle rising payments on a fixed income with our expert Brampton team. CMSpeople No Comments

Mortgage Rates & Bank of Canada 12 Jun 2026 Ontario Mortgage Rates: What Homeowners Need to Know This Week Confused about Ontario mortgage rates? Get the latest on the Bank of Canada rate hold, GTA housing market stats, and smart renewal tips. Aman Harish No Comments

Housing Market Updates, Mortgage Renewals 10 Jun 2026 How to Find Hidden GTA Housing Market Opportunities Find hidden GTA housing market opportunities in May 2026. Learn how new mortgage rules and market shifts can work in your favor. CMSpeople No Comments

Housing Market Updates, Mortgage Rules & Regulation 08 Jun 2026 How to Handle the 2026 Rental Mortgage Rules in Ontario Learn how to handle the 2026 rental mortgage rules in Ontario. Discover how the ban on double-counting income impacts you and how to scale anyway. Aman Harish No Comments

First Time Home Buyers, Housing Market Updates 05 Jun 2026 Will the Development Charge Reduction Program Lower Home Prices? Find out how the new Development Charge Reduction Program could lower pre-construction prices and make buying a new home in the GTA more affordable. CMSpeople No Comments

Housing Market Updates 03 Jun 2026 Is the GTA Housing Market Rebounding? May 2026 TRREB Stats Is the GTA housing market rebounding? Check out the latest May 2026 TRREB stats, average prices, and what it means for your mortgage. Aman Harish No Comments

Mortgage Rates & Bank of Canada 01 Jun 2026 Will the Canada Technical Recession Lower Your Mortgage Rate? Wondering if the Canada technical recession will trigger a Bank of Canada rate cut? Here is what it means for Ontario mortgage rates this June. CMSpeople No Comments

Mortgage Rates & Bank of Canada, Mortgage Renewals 29 May 2026 Is the Mortgage Renewal Crisis Ending? What the BoC Says Will the mortgage renewal crisis finally end? The Bank of Canada's 2026 report has answers for Ontario homeowners facing renewals. CMSpeople No Comments

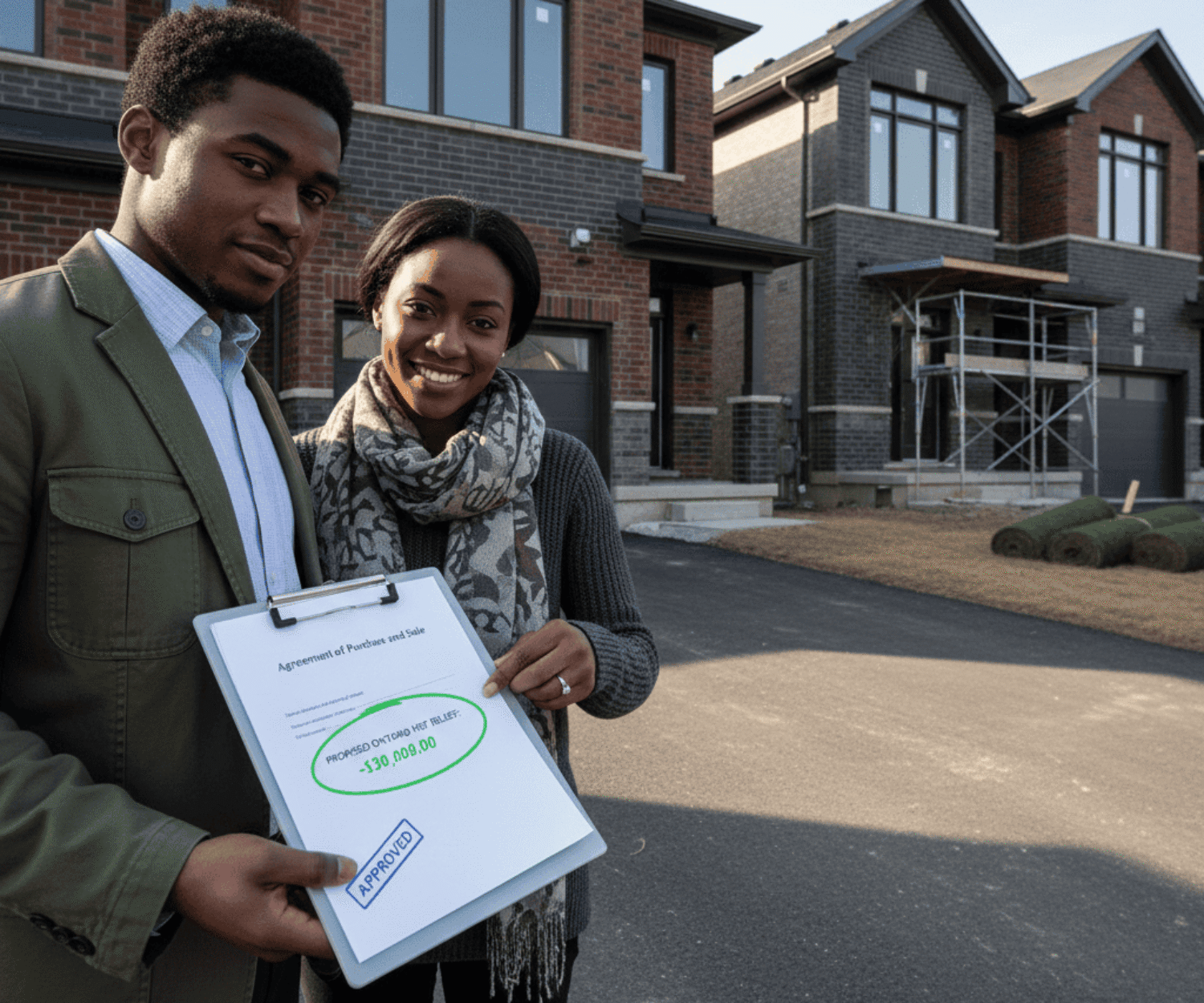

First Time Home Buyers, Housing Market Updates 27 May 2026 How to Save $130,000 with the Ontario HST Rebate Learn how the new Ontario HST rebate offers up to $130,000 in tax relief for GTA pre-construction buyers. See if you qualify and how to maximize savings. Aman Harish No Comments

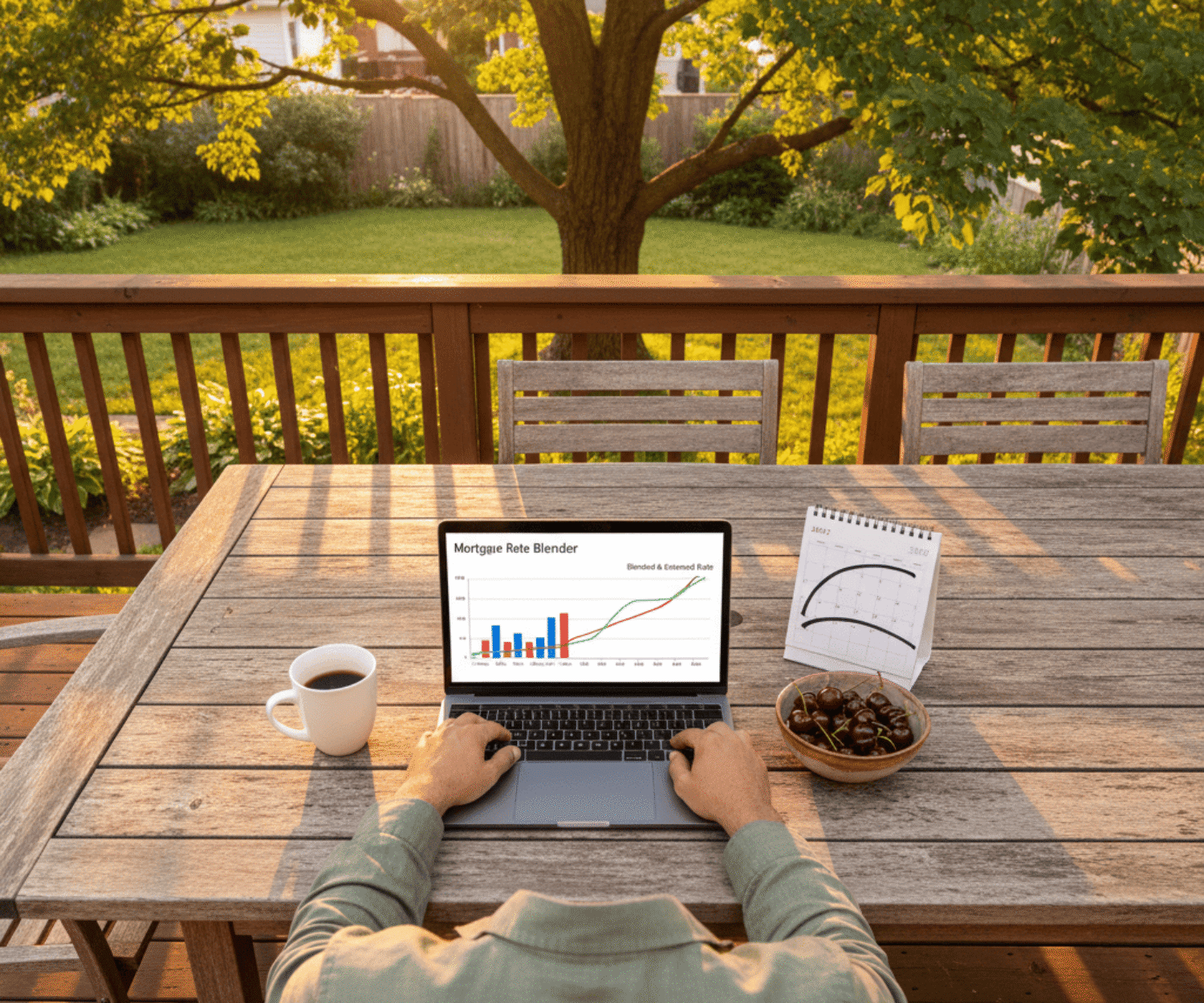

Mortgage Renewals 25 May 2026 Should You Get a Blend and Extend Mortgage in 2026? Facing a mortgage renewal in 2026? Learn how a blend and extend mortgage works, its pros and cons, and if it can save you from high prepayment penalties. CMSpeople No Comments

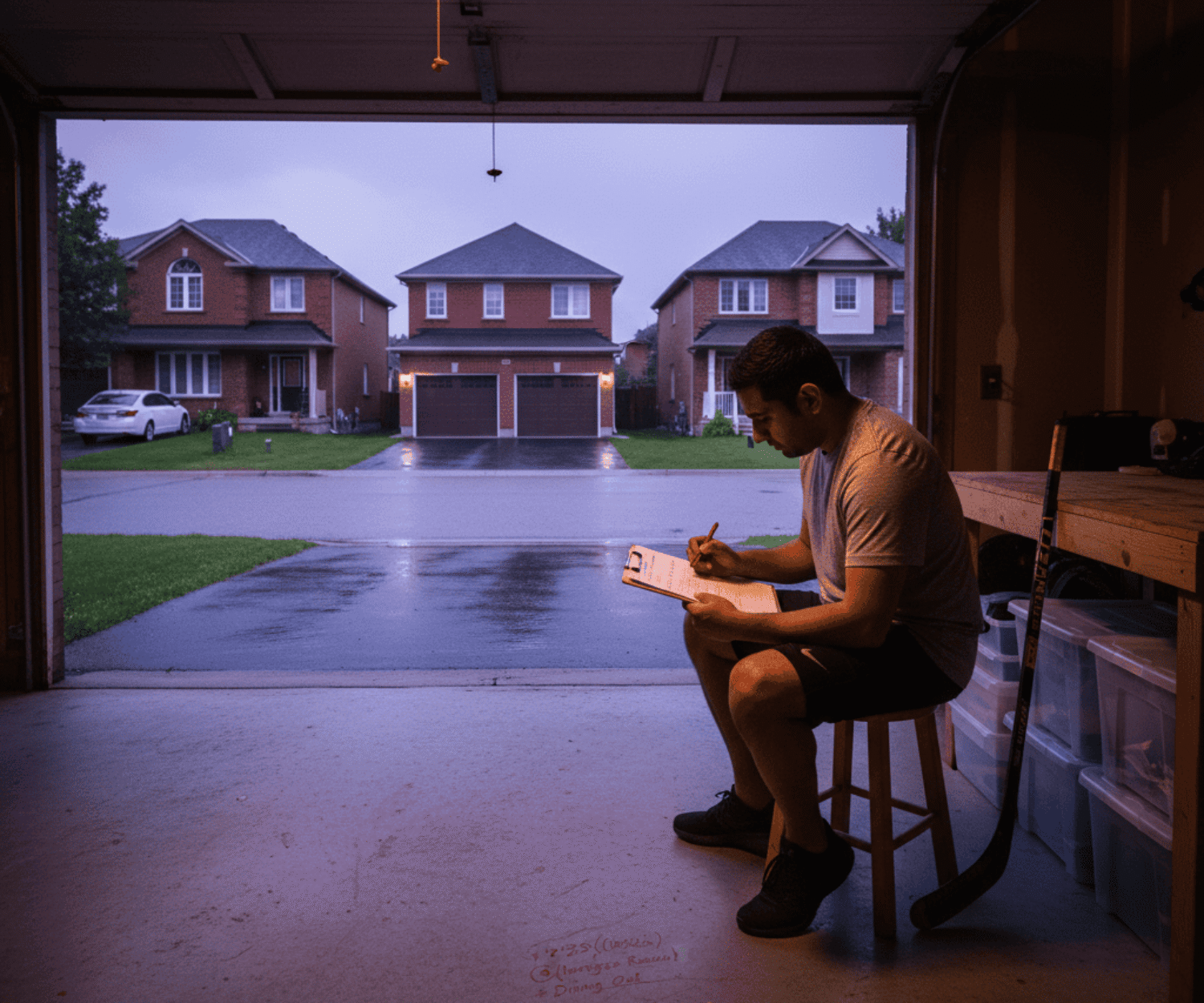

Mortgage Renewals 22 May 2026 How to Survive a $375 Payment Hike on Your 2026 Mortgage Renewal Facing a 2026 mortgage renewal? CMHC reports payments are up $375 on average. Here is how Ontario homeowners can beat the rate shock and save money. Aman Harish No Comments