Navigating Mortgage Rates in 2025: A Look Ahead

The mortgage landscape in Canada has been dynamic, to say the least. As we move into 2025, it’s crucial to understand the factors influencing mortgage rates and how they might impact your homeownership and overall mortgage journey. This blog post, based on insights loosely formed from various mortgage rates forecasts and sources, delves into the current market conditions and offers a perspective on where rates may be headed. Whether you’re a first-time homebuyer or looking to renew your existing mortgage, understanding the mortgage market is essential.

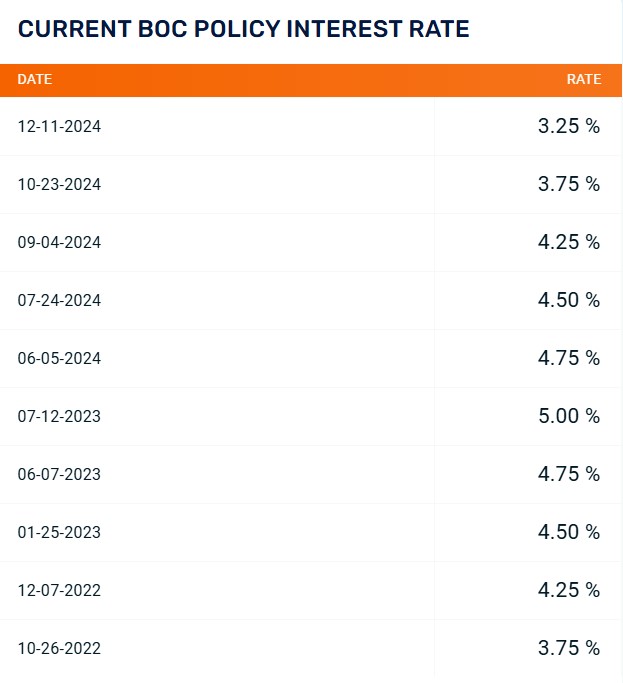

Recent Rate Cuts and the Bank of Canada’s Position

The Bank of Canada (BoC) initiated a monetary easing cycle in June 2024, after reaching a 23-year high of 5.0%. Since then, we’ve seen significant rate reductions, including a substantial 0.50% cut in December 2024. This brought the policy rate down to 3.25%, offering some welcome relief to borrowers concerned about their mortgage payments. See below for a chart with the history of rate increases and decreases since October 2022.

The BoC’s primary goal is to bring inflation back within its target range. While inflation has cooled, various factors are complicating the central bank’s path. These include a strong December 2024 job report, a weakening Canadian dollar, and the potential impact of U.S. tariffs. This makes accurate mortgage rates forecast more challenging.

Economic Uncertainties and Their Influence on Rates

Several economic factors are creating uncertainty in the mortgage market. Canada’s economic recovery remains fragile, particularly in the face of potential U.S. tariffs. High household debt, weaker labor markets (despite a positive December report), and wavering consumer and business confidence add to the complexity. The political landscape, with a new U.S. President and an outgoing Canadian Prime Minister, further clouds the outlook and makes creating a precise mortgage rates forecast difficult. Many are turning to a mortgage broker for guidance during this uncertain time.

Despite these uncertainties, the BoC is expected to continue lowering its policy rate. The weaker Canadian dollar, currently trading below 70 cents U.S., is expected to decline further, adding another layer of complexity. This will have a cascading effect on all aspects of the mortgage market.

Key Economic Indicators

Several key economic indicators are playing a crucial role in shaping the BoC’s decisions, influencing not only the economy as a whole but also specific mortgage rates:

- Inflation: Headline inflation has declined, reaching 1.9% in November 2024. However, the cost of essential goods like rent and food has increased significantly over the past three years. This continued pressure on household budgets will influence how people interact with the mortgage market.

- Labour Market: The December 2024 job report showed unexpected strength, with a decrease in the unemployment rate and a significant gain in jobs. However, wage inflation has slowed. These labor market dynamics play a role in affordability and therefore are relevant to any mortgage rates forecast.

- Economic Growth: While October 2024 saw slightly better-than-expected growth, November’s GDP contracted. Overall economic growth is projected to be underwhelming. Stagnant growth impacts investment and influences potential mortgage demand.

- Housing Market: The housing market has shown signs of warming in response to recent rate cuts. However, concerns remain about potential price pressures and affordability. This activity is what those producing a mortgage rates forecast keep top of mind.

- U.S. Economy: The U.S. economy and its rate-cut pace significantly impact Canada. The incoming U.S. presidency introduces uncertainty, particularly regarding trade and potential tariffs. This uncertainty contributes to the complexity of the mortgage market and challenges in producing an accurate mortgage rates forecast.

Predictions for 2025

Despite the complexities, it’s anticipated that the BoC will continue cutting rates in 2025. A further 0.75% in cuts is predicted by the end of the year, bringing the policy rate down to 2.50%. This would result in a total prime rate drop of 2.5% by the end of 2025, which would have substantial implications for anyone with a mortgage. A chart below illustrates projections for the next 8 quarters. Consulting with a mortgage broker can help you navigate these fluctuations.

Fixed vs. Variable Rate Mortgages

Fixed mortgage rates are influenced by the Canadian bond market. Recent bond yield volatility suggests that fixed rates may not decline significantly in the near term. Variable mortgage rates, on the other hand, have more room for decline and are likely to offer more significant savings as prime rates decrease.

Mortgage Advice for 2025

In this dynamic market, shopping around for the best mortgage rate and product is crucial. Consider a variable rate mortgage to take advantage of potential rate cuts. If you’re concerned about rate fluctuations, you can always lock into a shorter fixed-rate term mortgage. A reputable mortgage broker can help you find the best deal. This is particularly important with the current mortgage rates forecast.

Conclusion

The mortgage market in 2025 is expected to be influenced by various economic and political factors. While uncertainties remain, the overall trend points towards further rate cuts by the BoC. Staying informed and seeking expert advice, perhaps from a trusted mortgage broker, is essential to navigate this complex landscape and make the best mortgage decisions for your individual circumstances. Anyone can arrange a mortgage, but not every mortgage broker will be experienced enough to understand the economic impacts on the housing and mortgage market and in turn, guide you accordingly. Remember to consider all your options, including variable and fixed rates, and take advantage of available resources and expert advice to secure the best possible mortgage for your needs. Keeping an eye on any mortgage rates forecast will be beneficial.